Financing the Care Sector | Here's what you need to consider

This article takes a focused look at the financial markets that support the Care sector, considering the current funding landscape and sentiment in the market.

For the last two years, writing any kind of blog or opinion on the care sector and its supporting financial markets has been somewhat of a challenge. A rapidly changing landscape with political, economic regulatory and global issues all influencing the facets within the day-to-day operations of a care business.

The sector, which delivers frontline service and care to people who can be at their most vulnerable, constitutes a vital part of the healthcare provision in the UK. It has been well documented that the UK has an aging population, with higher needs and earlier diagnosis of conditions leading to support. Alongside subsequent referrals, there is an increase in demand on providers. Christie & Co data suggests that by 2034, 21% of the population could be over 65, equating to 16 million people.

Financing the Sector

When exploring funding, any operator or new entrant has to consider the noise that is in the sector, whether it is regulatory, economical or political.

Existing Operators

Established operators will see opportunities in potential homes to improve them or increase their value. If this is to be the case, due diligence must be done, in most instances clear financial forecasts and operational strategy will be essential for a successful lend.

More so than ever existing operators need to be prepared to act on a potential acquisition. Although in general terms lenders will not provide a “blank cheque”, from our experience we are supporting clients with an assessment of their current business alongside any potential target, providing confidence to agents and sellers that offers are deliverable.

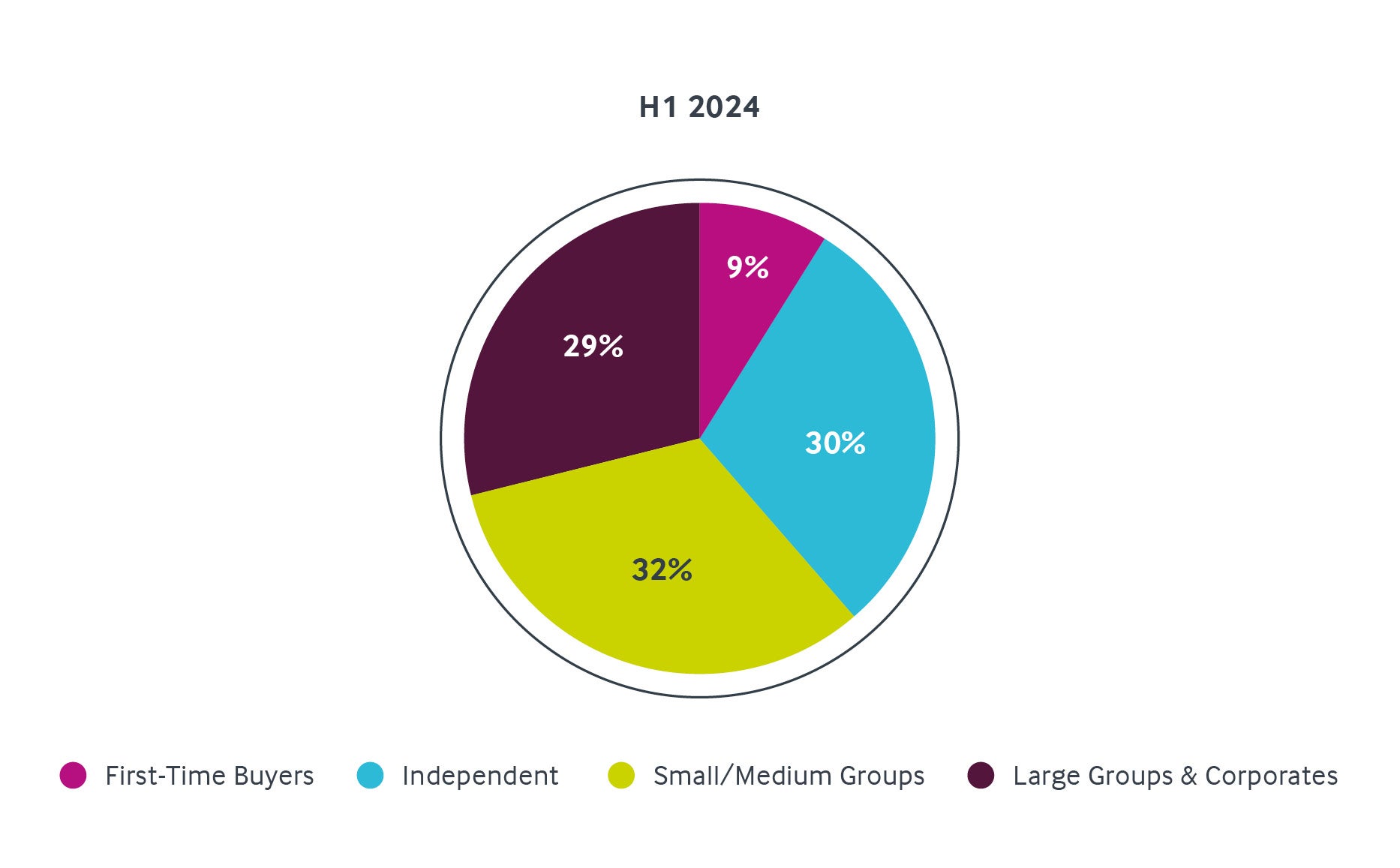

According to Christie & Co’s market analysis, supply and demand is increasing, especially for the small to medium groups. 63% of completions of care homes in the first half of 2024 were between the 20 to 59 beds, subsequently being sold to 30% independent and 32% small to medium groups.

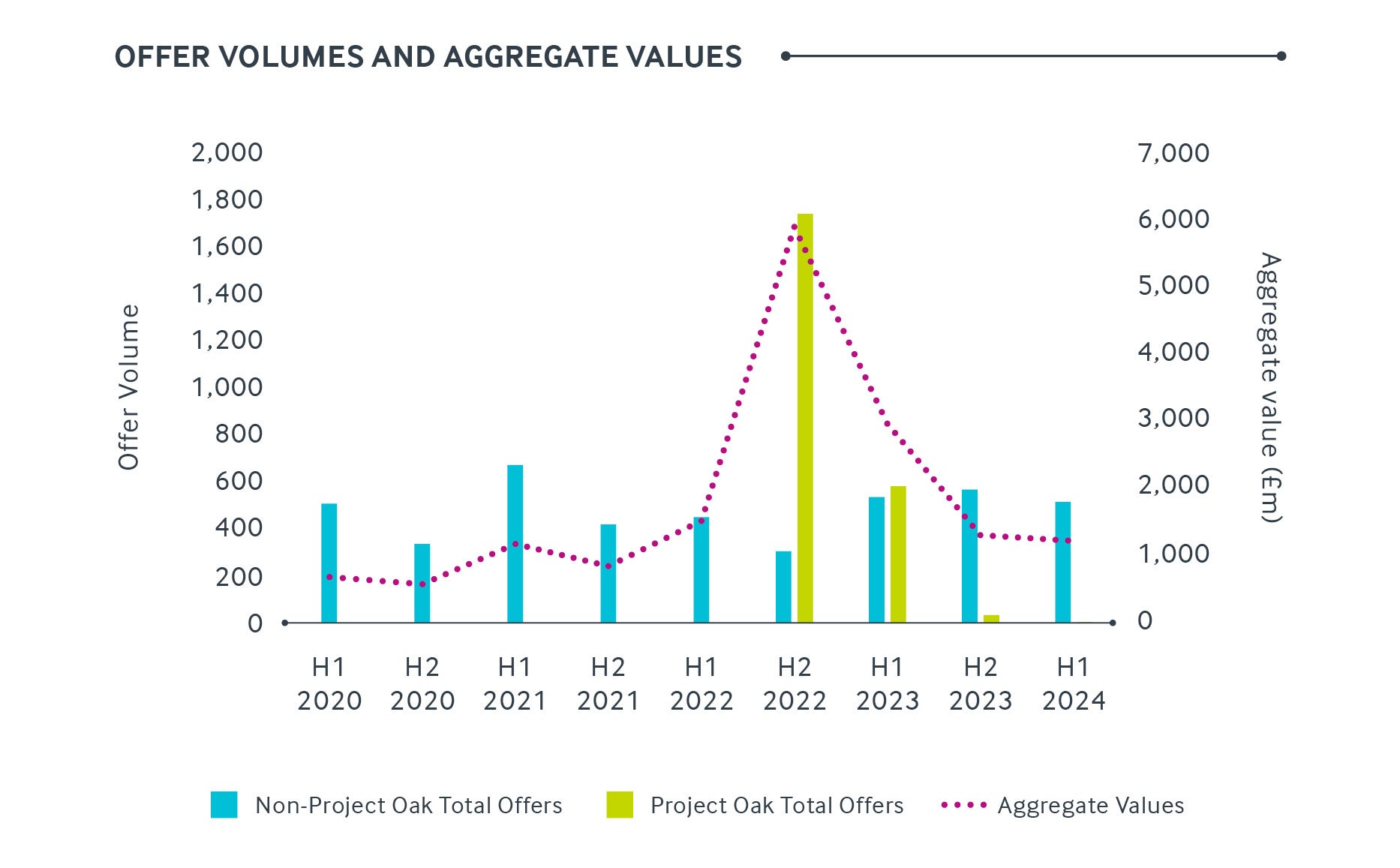

The supply of homes into the market between 20 – 59 bedrooms has remained consistent, however the demand from operators to acquire has increased by 11% year on year, from 38% in 2023 to 43% in 2024. Typically, these operators will be wanting to acquire the larger homes of 35+ beds, potentially a better quality than their existing assets.

This strategy of acquisition and demand is further supported by Christie & Co data through 2023, and H1 of 2024, remaining at its highest since 2021.

This demand has caused values to remain solid and multiple bids on targets. When seeking to expand portfolios, operators will need to be well prepared with funding strategy. This is an area where Christie Finance has supported multiple clients, making sure they are financially fit to acquire.

New Entrants

For new entrants the key areas to focus on will be the quality of experience or management team. Lenders will seek confidence in how well a new entrant can operate their first acquisition, what their career history is and what direct experience they can bring.

The next focus should be on the target acquisition. What is the quality of the current service provision? What is the regulatory rating? What is the financial performance? Is the current management and senior management remaining?

The funding market is still challenging to navigate for first time buyers, however we have supported many to acquire their first home. Preparation is key to a successful funding application. A lot of our process is to fully understand a clients’ plans with any potential target.

Key Takeaways on the Market

Overall, the sentiment and transactional analysis from Christie & Co Care Market Review suggest the market remains buoyant, however there is an increasing supply pressure for potential buyers. There has been a decrease in first time buyers, which could be due to the decrease in homes below 20 beds and lack of medium providers being able to acquire or upgrade their portfolios, thus disposing of their smaller assets.

The finance market has continued its cyclical nature, with funders changing policies, exiting and returning. This makes acquiring debt always a challenge, before even getting into the detail of operation, structure, affordability, regulatory and quality of the asset.

Over the past 12 months we have seen the Bank of England Base rate continue to fall, alongside contracting debt margins.

Appetite remains strong to support the sector, but heightened due diligence and lack of understanding by lenders can sometimes frustrate and protract credit decisions. The ability to make yourself fit to buy by fully understanding not only the sector, structure of debt, the available funders and the terms that could be available to you will enable you to act quickly when offering on target.

Christie Finance’s detailed understanding of the sector and finance landscape helps to support clients with funding arrangements to achieve their aspirations whether it is to enter the market, grow their portfolio, refurbish or re-invest.

Christie & Co released their 2024 Care Market Review in October, analysing a range of topics relating to the UK healthcare business market, include capital markets, land and development, the transaction market, shifts in local authority fee rates, operator sentiment, and a Q&A with Matt Lowe (CEO at LNT Care Developments).

To read more on Christie & Co's Care Market Review, click here: https://www.christie.com/news-resources/publications/care-market-review-2024/

To find out more, get in touch:

Jimmy Johns

Director of Corporate Debt Advisory - Healthcare

M: +44 7711 767 593

E: jimmy.johns@christiefinance.com